As the economy improves, mortgage rates could dip as low as the 4% range, bringing buyers back to the market.

The inflation rate has been calming in recent months, contributing to falling mortgage rates through the holidays. Consumer prices are still running well above the typical 2% inflation rate, but November’s level of 7.1% was the lowest in 2022. Decelerating inflation is the key reason for the forecast of a 5.5% mortgage rate by the second half of 2023. Should the deceleration speed up faster than expected, the possibility of mortgage rates in the 4% range exists—which would bring buyers back to the market.

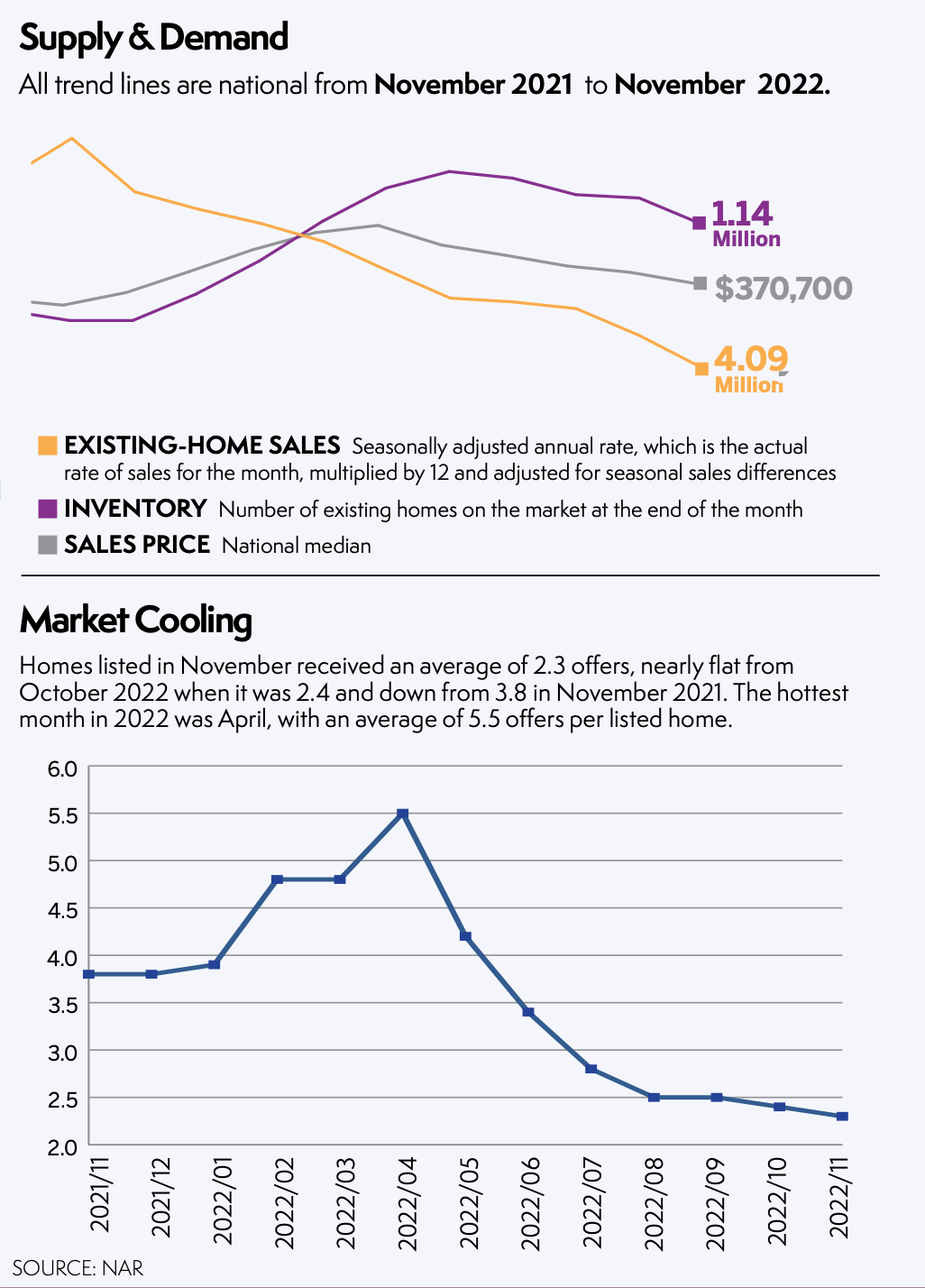

A significant potential contributor to the continuing decline in inflation is the rent people pay and the equivalency in rent owners would have paid. These measures are still on accelerating paths, with annual gains of 7.9% and 7.1%, respectively—their highest rise since the early 1980s. These huge gains are a result of the housing shortage and historically low rental vacancy rates. But lagging data shows the housing shortage is not as acute as previously thought. The rental vacancy rate was 6% in the third quarter of 2022, up from 5.8% a year earlier, and overall sale inventory is up 2.7% in December. Data on new lease rates from apartment property managers show a marked slowdown in gains.

Moreover, multifamily housing starts—which are primarily apartments—hit 550,000 units in 2022, the highest in nearly 40 years. Apartment vacancy rates will undoubtedly rise further. Rent growth will surely slow. Overall, consumer prices will calm down even further.

In addition, NAR has advocated for converting vacant commercial space (empty shopping malls or office buildings, for example) into residential units through funding and/or tax credit incentives. Financial incentives to rehab dilapidated, abandoned homes in some major cities will also help bring about more housing supply and greater neighborhood safety.

As to the economy, there could be a recession—or maybe not. GDP is sliding along the near-zero growth line, but strong job creation is a bright spot. Despite layoffs in some industries, overall job openings still exceed the number of unemployed by a 7-to-1 ratio. Net job creation will be around 1 million to 2 million this year. The people who take those jobs are future homeowners.

First-Time Buyer Share Still Low

Only 28% of home sales in November were by first-time buyers. That’s unchanged from October but up from 26% in November 2021. NAR’s 2022 Profile of Home Buyers and Sellers, released in November, found that the annual share of first-time buyers was the lowest since NAR began tracking the data.

©National Association of REALTORS®

Reprinted with permission